Efficient Market, or How Algo Dies

In March, after a spike in volatility, I turned off the futures bots. And that was probably the best decision I've made since 2018.

The reason for the algo bots' death is banal — low interest rates and high dividends kill volatility and, of course, trends.

Colleagues/competitors aren't showing inspiring results either. Only a couple of managers demonstrate good returns.

But the portfolio bot for stocks remains. And it shows good results. If you compare the volatility of IMOEX and RTSI, you'll see that short-term volatility in RTSI is higher, while long-term volatility is low (I used 5- and 20-day periods for calculations). In other words, using algo portfolios for futures means earning rarely but significantly. Even from my own experience I remember — you sit in a drawdown for a couple of months, then bam, and you've recovered the drawdown in a single volatile day. Trading slow bots in stocks is the opposite — most of the time you trade in a small profit. But when volatility rises (which usually happens during panics and downturns), you catch a moderate loss on the account.

This suggests a solution. Namely, trading algo in stocks using some kind of hedge. For example, in the form of a slow bot for RTS or an option structure. I'm not considering classic hedges because I don't believe in their effectiveness.

Another superstition from the algo world I've stopped believing in — diversification. And this mostly applies to futures. The Russian futures market consists of just three futures — RTS, SI, and SBRF. Two of these futures correlate, the third has an inverse correlation. This is completely inadequate — what diversification can there be? Especially considering that the bots mostly trade on volatility. In other words, you can only earn during high volatility.

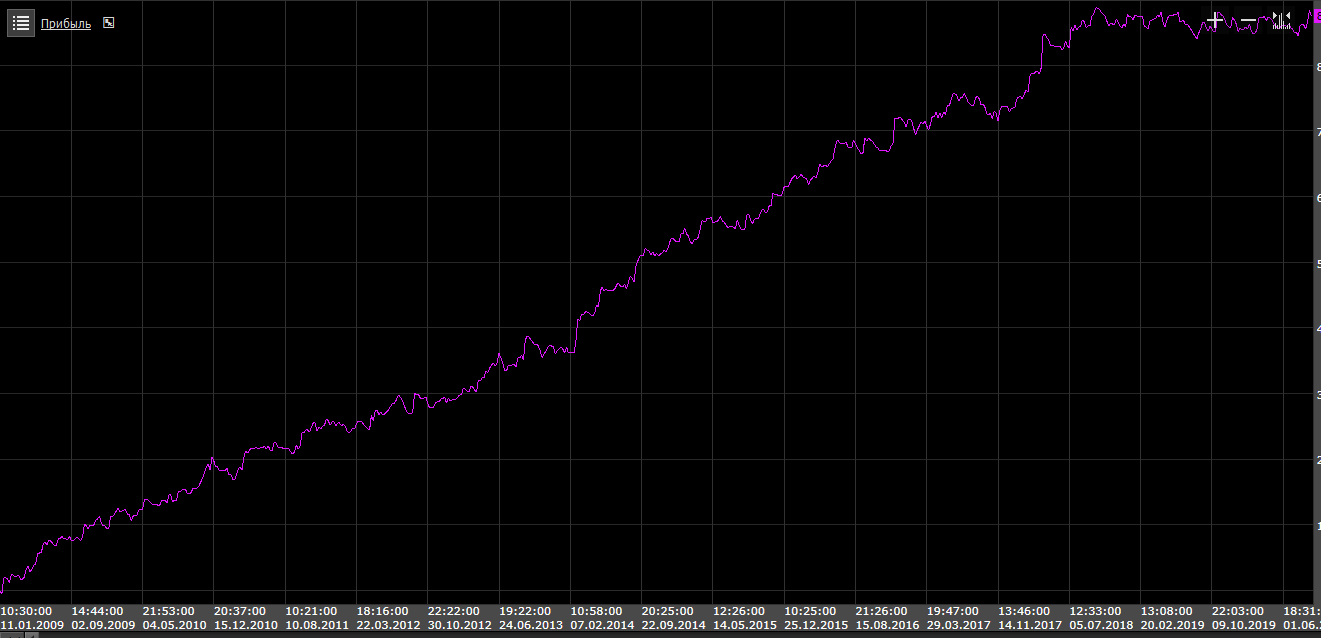

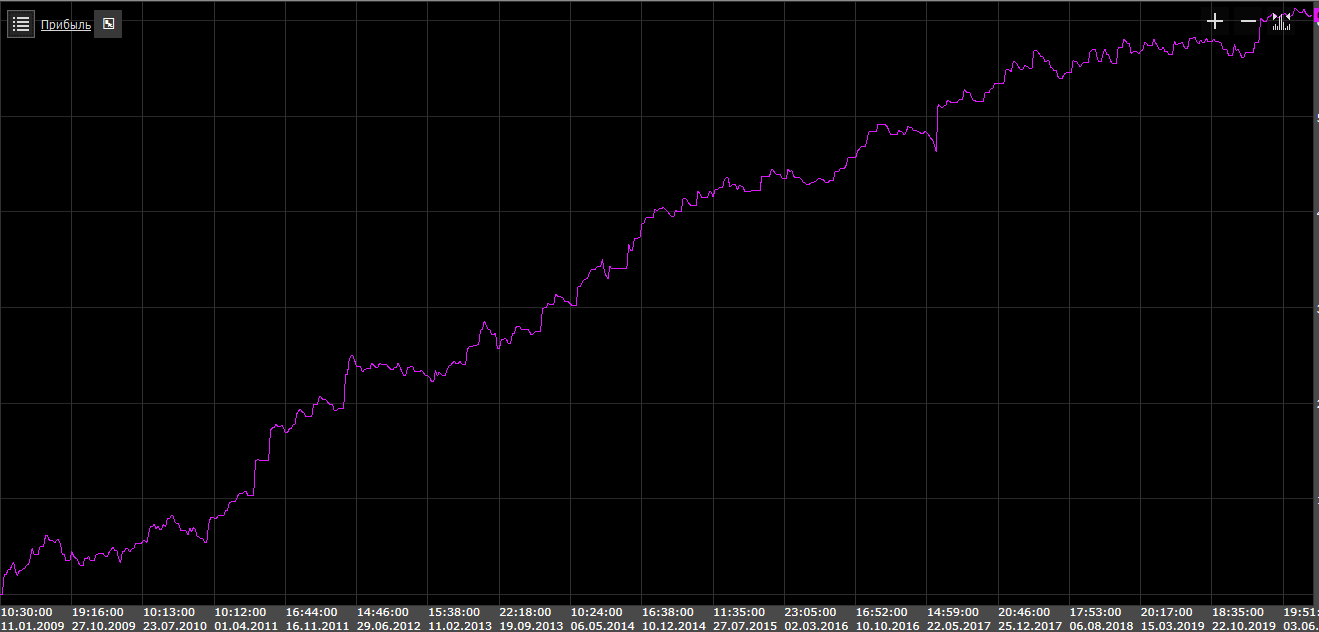

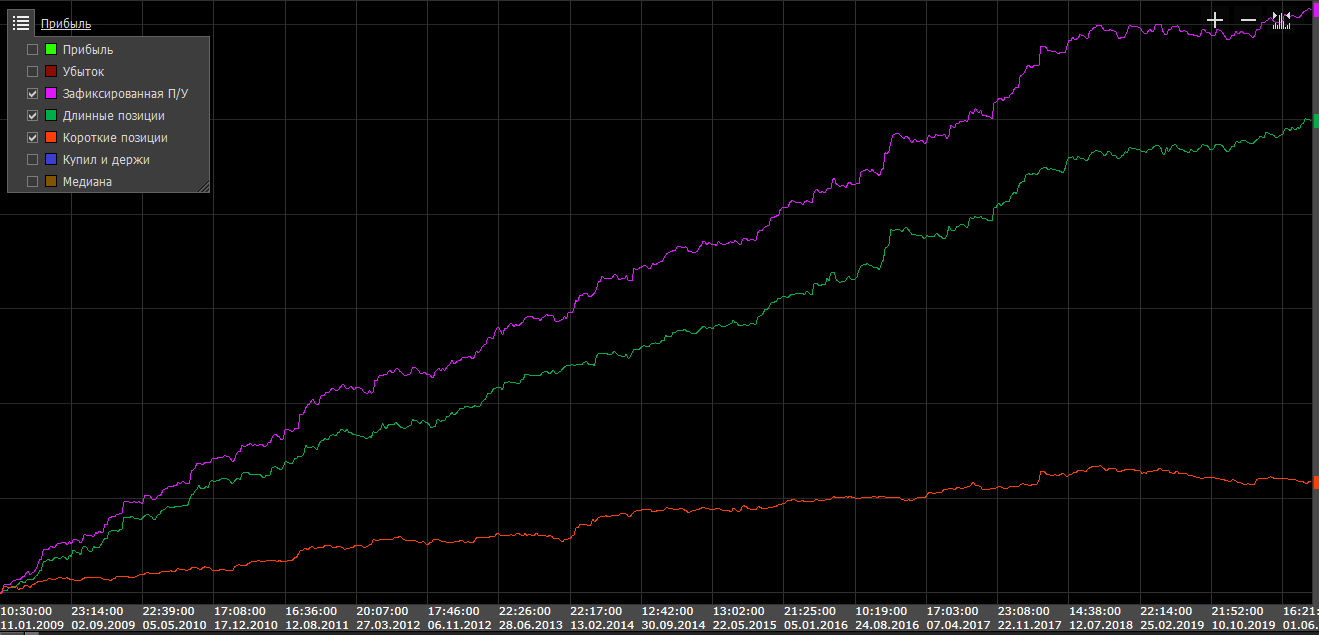

Equity of systems:

Result without optimization, based on this model

RTS near highs, but drawdown duration is the longest of all. You can safely write it off.

SBRF is still in drawdown, but the duration hasn't exceeded the previous drawdown yet

SI. The growth rate is so slow you might as well throw it in the trash.

FORTS portfolio. Slowly growing due to long positions, however drawdown duration is the longest.

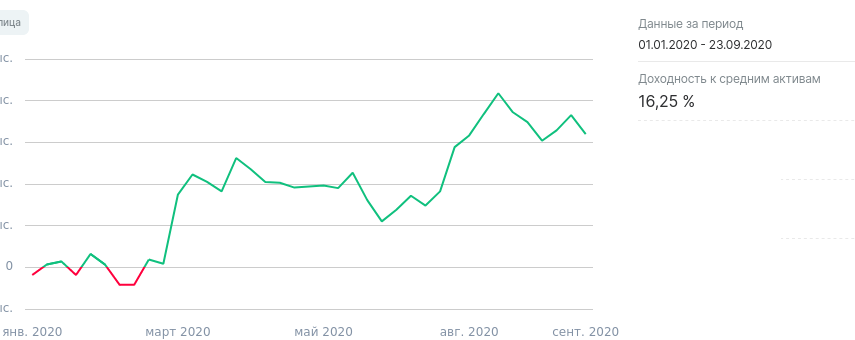

IMOEX portfolio (the model doesn't account for dividends and coupons from free cash)

And finally, the result for the current year. The IMOEX index is currently at -5.85%.

In conclusion, the following conclusion suggests itself — our market is becoming more efficient. It's becoming harder to make money on it. Previous models are dying. But on the other hand, the Moscow Exchange is introducing new instruments that open up new earning opportunities. For example, US stocks in rubles, or new derivatives. Every new instrument creates opportunities for arbitrage, investment, and speculation alike. The only thing I'd wish for is greater liquidity. There really isn't enough of it.